Chipotle Mexican Grill's (NYSE: CMG) price action is down in Q2 2025 for several reasons, including a post-stock split letdown, a significant CEO transition, global macroeconomic woes, and a sluggish 2025 outlook. However, those factors do not offset the company’s leadership position, quality management, fortress-like balance sheet, and substantial growth outlook.

While growth is impacted by forces outside of its control in 2025, Chipotle continues to gain market leverage with new store openings, including internationally, which is the driving force behind the share price in the long term.

Chipotle’s international expansion is starting to pick up momentum. The company opened two international licensed stores in the quarter, with more expected by year’s end. The company also recently announced plans to develop markets in Mexico.

The first location is expected by early 2026; add-ons will soon follow. Chipotle management views Mexico as a highly favorable market, as its ingredients and cooking style naturally fit.

Chipotle Falls on Strong Results, Tepid Guidance

Chipotle had a solid Q1, even with growth slowing to only 6%. The revenue came in at $2.9 billion, slightly below the analysts' consensus, with growth driven entirely by opening new stores. The company added 57 for the quarter, an 8.7% gain compared to last year. A slight decline in comps offset the increase in store count, at -0.4%, due to lower transaction volume.

Chipotle’s guests may visit less frequently, but they spend more. Average check increased by nearly 2%.

Margin news is mixed but ultimately favorable to investors. The company’s restaurant-level operating margin contracted by 130 basis points due to increased F&B and labor costs, but this was offset by reduced SG&A at the corporate level. F&B costs are up due to a combination of inflation, usage, and mix, while labor costs are rising due to inflation, higher minimum wages in California, and the deleveraging of comp sales.

The critical takeaway is that SG&A savings, both GAAP and adjusted, offset the increased restaurant costs, leaving adjusted net earnings up 7.4%.

Guidance is the headwind for the price action in 2025.

However, even with the expected impact of tariffs, the company forecasts a low single-digit comp store sales growth for the year and an increased store count. The store count is predicted to grow at a high single-digit pace, suggesting systemwide revenue and earnings growth in the low double digits at year’s end.

Chipotle Share Repurchases to Continue in 2025

Chipotle’s repurchase authorization is nearing completion in H1 2025, but investors can expect an increase soon. The company’s cash flow is sufficient to sustain a semi-aggressive pace while investing in new stores, and the balance sheet is a fortress.

The highlight at the end of Q1 reflects investments in 2024 and Q1, including reduced cash and equity. Still, the impact is negligible and offset by revenue, earnings growth, and a 1.5% share reduction.

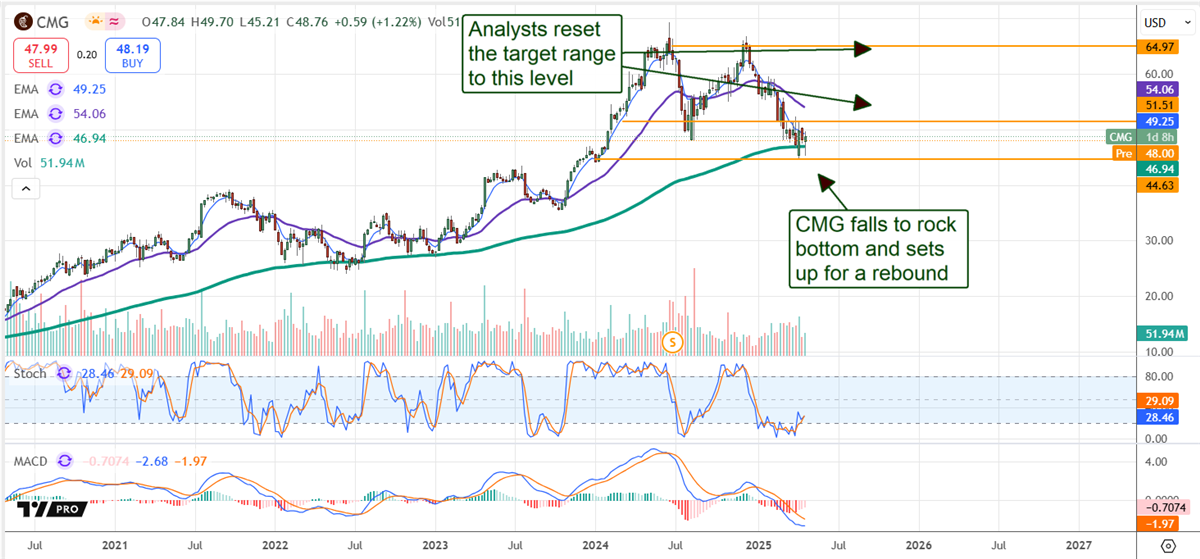

Analysts are lowering their price target for CMG stock following the Q1 release, but the market for this Moderate Buy-rated stock has already priced in the weakness. The reductions range from $55 to $65, offering a 22% to 44% upside from the critical support level.

The market for CMG is near that support level in late April and setting up for a rebound that could begin before the end of the quarter. Institutional buying activity aligns with the forecast for a stock price rebound, significantly outpacing sell volume, peaking in Q1 and remaining strongly bullish in early Q2.