When prospectors traveled west to California during the gold rush, many had no intention of doing any digging. Instead, they’d set up businesses selling digging equipment with the gold hunters as clients. Striking it rich while hunting for gold was rare, but the people selling picks and shovels made money no matter how successful their clients turned out to be. That’s where the popular investing term “picks and shovels” originated, describing a company that sold tools to people participating in the hot industry of the day. Right now, that hot industry is semiconductors, and the market is once again reaching new all-time highs. Today, we’ll look at three under-the-radar stocks that fit the definition of “picks and shovels” semiconductor plays.

Small-cap stocks can be risky, but they also tend to provide more upside than larger companies. Each of the following three companies has a market cap below $10 billion and a crucial service or component required in advanced semiconductor production. As the demand for chips and memory increases, so should the value of these stocks.

Camtek Ltd.: High Valuation Justified by Record Revenue

The semiconductor industry uses finely tuned processes to produce chips, and quality control is crucial to preventing losses.

Camtek Ltd. (NASDAQ: CAMT) is an Israeli-based developer of inspection and metrology equipment that has become a critical component for high-bandwidth memory (HBM).

HBM is technically demanding, requiring memory chips to be stacked to speed up processing. The closer the memory chips are, the faster they’re able to talk to each other and relay information. As AI compute demand increases, so will the need for faster memory processing.

Major memory companies like Micron Technology Inc. (NASDAQ: MU) are developing HBM4 stacks, the next generation of fast-processing memory. These stacks are the most complex semiconductor memory chips to date, but their complexity requires state-of-the-art metrology tools to measure the microbe-sized distances between chips accurately. Camtek’s specialized 3D metrology tools can measure nanometer-level spacing between wafers, which will become increasingly important as memory chip stacks get higher and denser.

Camtek’s recent earnings and guidance projections indicate this trend will benefit its bottom line well into 2027. In the company’s Q4 2025 earnings release, management reported record full-year revenue of $496 million and net income of $159 million, the latter up 15% year-over-year (YOY). Camtek projects another double-digit growth year in 2026, with Q1 2026 guidance of about $120 million. Management expects revenue to pick up significantly in the second half of 2026 as HBM4 chips roll out from major suppliers.

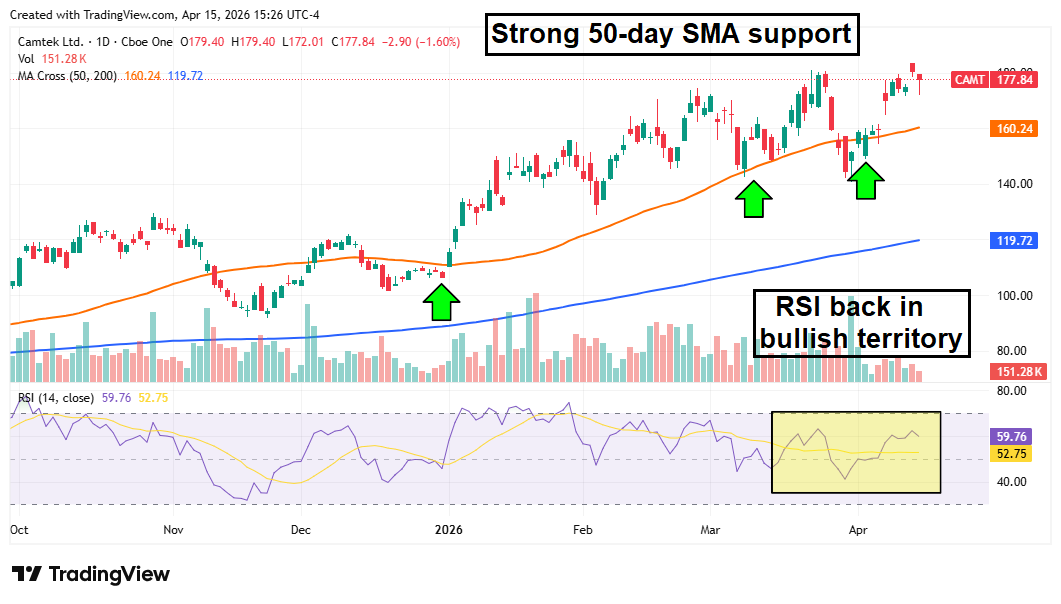

CAMT shares also have a very optimistic-looking chart. The stock has strong support at the 50-day moving average, and the Relative Strength Index (RSI) has once again flipped bullish. The momentum behind this uptrend is strengthening, and there appears to be plenty of upside still on the table.

Silicon Motion Technology: Still Undervalued Despite 50% YTD Gain

A direct beneficiary of the memory shortage, Silicon Motion Technology Corp. (NASDAQ: SIMO) is a Hong Kong-based developer of NAND flash controllers.

NAND memory devices are another crucial component for AI hyperscalers, and Silicon Motion is also setting revenue records. The company’s Q4 2025 revenue of $278 million represented a YOY increase of more than 40%, and gross margins reached the high end of guidance projections at 49%.

The Q1 2026 report is due on April 28, and management projects revenue of $292 million to $306 million. Despite setting revenue records, the stock still trades at 39X earnings, below the semiconductor and overall tech sector averages.

SIMO shares are still up more than 50% YTD despite a pullback during the first month of the Iran war. But now that semiconductor stocks are rallying again, SIMO has retaken its 50-day moving average.

The bullish momentum is confirmed by a cross on the Moving Average Convergence Divergence (MACD) indicator, and new all-time highs appear on the horizon.

Kulicke and Soffa Industries: Earnings Beats Boosting Stock to New Highs

Kulicke and Soffa Industries Inc. (NASDAQ: KLIC) is the best-performing stock on our list YTD, up over 80% so far in 2026. The Singapore-based company provides die and wire bonding services for semiconductor packaging, and earnings have supported its recent stock surge.

The company reported $199 million in revenue during its Q1 2026 release, up more than 20% YOY and easily beating analysts’ estimates. Management also reported impressive growth in the company’s fluxless thermo-compression bonding (TCB) and expects TCB revenue to top $100 million during fiscal 2026.

Q1 gross margins of 49.6% also surpassed expectations, and, like Silicon Motion, the company projects a strong finish to the year.

KLIC shares broke out of a month-long consolidation pattern in April and have now rallied to new all-time highs. Despite the 80% YTD gain, the upward momentum is gaining steam, with a bullish MACD cross bolstering the technical tailwinds. The company’s next catalyst comes on May 5 when it reports fiscal Q2 2026 earnings.