The raging semiconductor rally received another boost this week when UBS analyst Timothy Arcuri raised his price target on Micron Technology Inc. (NASDAQ: MU) to a stunning $1625, nearly triple its previous target.

The stock was trading under $800 at the time of the upgrade, so the new target represented an upside of more than 100% and a company valuation of over $1.8 trillion.

MU shares rallied nearly 20% the following day, and the entire industry seemed to join in, as the iShares PHLX Semiconductor ETF (NASDAQ: SOXX) accelerated 6%.

When the entire industry seems to rally every day, it's easy for undeserving companies to get caught in the wave and soar to new all-time highs. But it's also crucial to remember Warren Buffett's quote about what happens when the wave recedes: you find out who’s been swimming without proper attire.

Why UBS Boosted Their MU Price Target by 200%

Arcuri’s May 26 MU price target boost reflected his view that high-bandwidth memory (HBM) is undergoing a fundamental shift from a cyclical semiconductor business to one driven by long-term AI infrastructure demand.

Instead of a cyclical manufacturing industry, HBM now has structural growth tailwinds led by two key factors:

-

Long-term Revenue Visibility: AI hyperscalers are running into HBM backlogs and are more willing to lock in long-term agreements for supply and access to next-gen products. Micron already has agreements in place for its entire 2026 HBM supply.

-

Concentrated Supply Chain: Producing HBM products at a large scale is a capability currently possessed by only three companies: Micron, Samsung Electronics Ltd. (OTCMKTS: SSNLF), and SK Hynix. In its Q1 2026 earnings report, Micron projects that data center demand for HBM will exceed $100 billion by 2028, more than three times the $35 billion in HBM sales to data centers in 2025.

Given these secure, long-term agreements and heavy supply concentration, Arcuri argues that MU shares are worth a valuation similar to NVIDIA Corp. (NASDAQ: NVDA). However, the stock traded at under 10x forward earnings at the time of the call—far cheaper than the NASDAQ 100 average of 24x earnings, hence the massive re-rating.

3 Stocks Rallying in Sympathy: Hype or Substance?

Many tech stocks in the AI and semiconductor space rallied hard in sympathy, especially Western Digital Corp (NASDAQ: WDC), Rambus Inc. (NASDAQ: RMBS), and onsemi (NASDAQ: ON). But are these gains warranted? Despite the industry's exuberance, each company still requires substantial due diligence to separate substance from hype.

Western Digital: A Clean Complement to Micron’s Surge

Western Digital Corp also rallied 8% the day of the report, bringing its total year-to-date (YTD) gain to over 200%.

Western Digital is now a pure hard disk drive (HDD) manufacturer following the SanDisk spinoff, and the same logic that UBS applied to Micron’s HBM products also applies to Western Digital’s HDDs.

Hyperscalers are locking in long-term agreements, and the company’s production capacity throughout 2026 has already been claimed. The fiscal Q3 2026 earnings report on April 30 confirmed the bull thesis with a massive double-beat featuring 45% year-over-year (YOY) revenue growth and gross margins over 50%.

Several technical staples underpin the lengthy rally in WDC shares. It has strong support at the 50-day moving average, which has traded above the 200-day moving average for over a year. A bearish crossover in the Moving Average Convergence Divergence (MACD) indicator briefly paused the rally, but now a bullish reversion appears to be underway as the stock makes new all-time highs.

Rambus: Undervalued Logic Company Licensing Necessary IP to Data Centers

Rambus is a classic “picks and shovels” play on the memory storage theme.

The company develops memory-interface systems that enable the GPU and memory stack to communicate within the data center mainframe, and licenses them as IP.

High-margin licensing products that can be sold regardless of which memory company wins the design provide a steady, recurring revenue stream.

Additionally, the firm’s HBM4E Memory Controller, launched in April, is now the industry's fastest. The stock has surged more than 60% YTD but remains undervalued relative to peers in the AI space.

RMBS shares have been more volatile than WDC, but volatility is often the price investors pay for higher upside. The stock spent two months stuck in neutral, bouncing between the 50-day and 200-day moving averages as the Relative Strength Index (RSI) remained in bearish territory.

However, an April rally sent the price above the 50-day moving average, and the momentum stalled when the RSI crossed above 50 into the bullish range. The 50-day moving average now appears to be support, which bodes well for future upside potential.

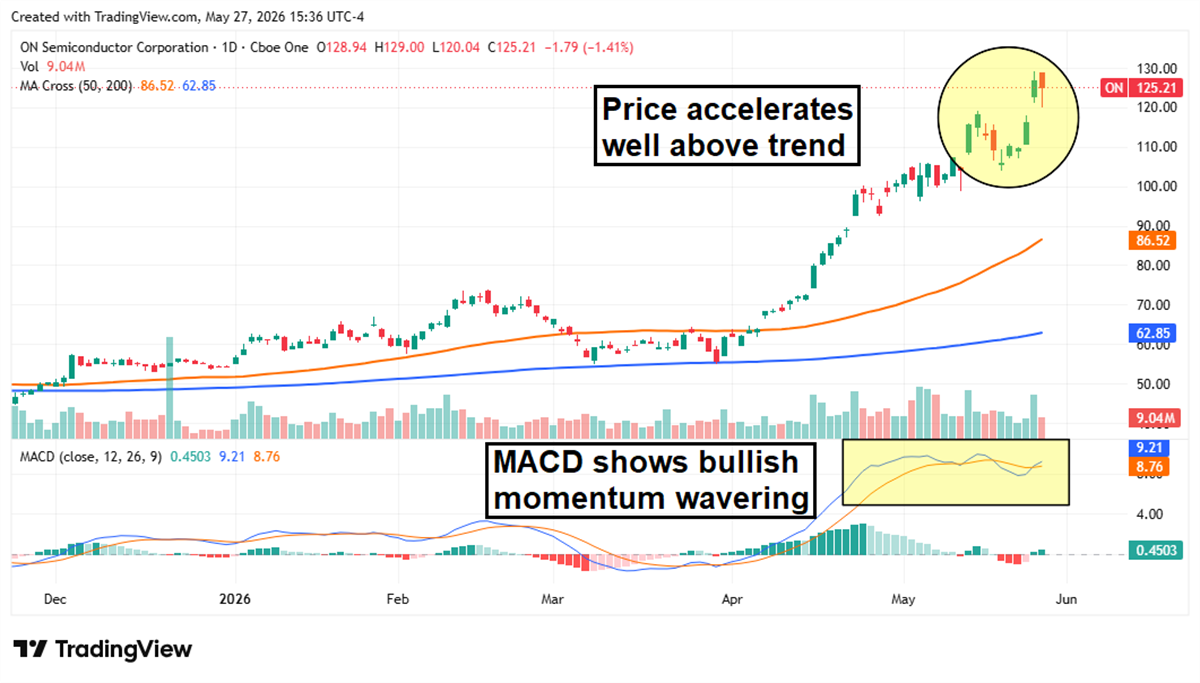

onsemi: Sympathy Rally Without the Substance

onsemi also rallied 9% on the day of the Micron report, but the UBS thesis doesn’t really apply here.

The company traditionally makes chips for the automotive and industrial markets, which are cyclical and not closely tied to the broader AI space.

onsemi has some data center business, but it accounts for only a small portion of the company’s total revenue. For example, the $797 million in Q1 automotive revenue was more than half of the company’s total Q1 2026 sales.

Management expects data center revenue to double YOY in 2026, but that’s still just $500 million out of a projected revenue base of more than $6 billion.

While the company has a compelling bull thesis of its own, it remains outside the Micron paradigm. And an almost 90% gain over the last three months has the stock looking frothy. The price is now well above trend, and the MACD is hinting that the bullish upswing is losing momentum. It might be a good time to take profits on ON shares.