Levi Strauss (NYSE:LEVI) did not have a great year despite the strong rebound that is already underway. The company saw its revenues decline... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| Written by Thomas Hughes Levi Strauss Is A Post-Pandemic Winner Levi Strauss Is A Post-Pandemic Winner

Levi Strauss (NYSE:LEVI) did not have a great year despite the strong rebound that is already underway. The company saw its revenues decline more than 60% in the 2nd quarter of the year and they have yet to regain the pre-COVID levels. And yet the analysts continue to warm up to this stock. Not because it is such a pandemic winner, it certainly isn’t that, but because it is set up to win in the post-pandemic world. The company has a great brand with global recognition, it’s making big strides into the eCommerce/direct-to-consumer arena, and the brick&mortar locations that it relies on are on the brink of a major, vaccine-supported reopening.

eCommerce Underpinning Results For Levi

eCommerce is not only helping Levi Strauss recapture lost revenue but it is juicing the bottom line as well. On a net basis, eCommerce sales improved 52% YOY in the 3rd quarter and drove a 60 basis point improvement in gross margin. This is important to note because many retailers/manufacturers relying on eCommerce have seen their margins squeezed by higher costs in the DTC channels. The takeaway is that eCommerce will not only aid growth as the company moves forward but that it will also leverage earnings.

CFO update, Q3 earnings report "The strength of the Levi’s brand is demonstrated in our gross margins, and revenues have been recovering from COVID-19 related disruptions faster than expected, driven by e-commerce, international and our women’s business, particularly within Europe and in the United States. Inventory is healthy headed into holiday, we are making investments in our digital transformation, and our cost and working capital actions have put us on a clear and accelerated path to achieving our adjusted EBIT margin 'North Star' of at least 12% when revenues recover to pre-COVID levels."

The Analysts Like What They See In Levi’s

The analysts like what they see in Levi’s despite the impact of the pandemic. Over the last 180 days the company has turned the few analysts sitting on the fence into bulls and they are driving the shares higher. The consensus target for Levi’s has risen $2.00 or more than 10% and this trend is not over. Guggenheim is only the latest bull to issue a price target increase and that a stout $4.00 to $24 or about 26% upside. Since the 2Q report was issued the stock has gotten 7 nods from the analyst community include 3 upgrades and 7 price target hikes.

The most impactful upgrade came from Goldman Sachs. The analysts at Goldman Sachs switched from bear to bull raising the rating from sell to buy and setting a target of $23. According to them, Levi’s is delivering on several initiatives including the DTC channels that promise to drive increased sales, higher margins, and EPS growth. The analysts at Bank of America echo that sentiment calling out the stock as an underappreciated COVID-recovery story with underlying brand strength.

The Technical Outlook: Levi’s Broke Out, New Highs Are In Store

Shares of Levi’s made a stunning recovery led by the analysts and their upgrades. The stock gained nearly 85% before hitting its peak and has since retreated back to a firmer level of support. Now, with the analyst’s sentiment coming to a boil, the stock looks like it could retest the recent high if not set new highs very soon. In the near-term, price action may continue to falter and/or test support near the 30-day EMA. The indicators are bearish and suggest price weakness will continue. That said, so long as the price action remains above the EMA the uptrend is intact and falling indicators a good thing.

Read This Story Online Read This Story Online |  A major regulatory shift is scheduled to take effect this July — and it could have serious implications for your financial future.

Big Banks are already positioning themselves to benefit from it…

This new policy allows them to treat a certain asset as equivalent to hard cash.

They're now placing more trust in it than in stocks, bonds, or even the U.S. dollar itself.

Using an IRS-approved strategy, it's possible to convert retirement funds into physical gold — with no tax penalties. Send Me the FREE Presidential Gold Guide |

Written by Thomas HughesTailwinds Will Drive Growth For Retail In 2021

Retail (NYSEARCA:XRT) has been one of the hottest and most unexpected trends of the pandemic. The shut-downs forced us to stay home, in response we spent our travel and leisure money on stay-at-home consumer goods, and there has been nothing but positive tailwinds since. The number one tailwind was economic stimulus but even that was only a boost to trends that were already in place. The trend I speak of is labor market improvement, a trend that has resumed in the wake of the summer’s economic reopening.

The American consumer was very healthy before the pandemic began because jobs were abundant and wages were rising. When the pandemic struck the American Consumer didn’t wither and die. While some were hurt badly by it many others adjusted to the new life kept on working and banked a lot of the stimulus. Or else used it to upgrade their lifestyles which ultimately means spending money and greasing the economic wheels.

Now, with unemployment down more than 50% from the summer peak and expected to shed another 3% to 4% over the next two quarters there are new tailwinds arising for both the consumer and the retail sector. These come in the form of renewed stimulus and a vaccine-supported reopening that will only spur retail spending to new heights.

Tractor Supply Company Is A Household Name

Tractor Supply Company (NASDAQ:TSCO) is not a small business but it is one that failed to garner much spotlight. Perhaps it’s the name, Tractor Supply Company because this company is closer to a high-tech general store than it is to a tractor dealership. That all changed when the pandemic struck. The company reported high-double-digit increases in revenue that were driven by both customer growth and ticket averages that are expected to remain sticky into the coming years. The growth will be supported by store expansion as well, expansion into underserved and more-rural areas where Target and Walmart have yet to venture.

In terms of dividend, Tractor Supply Company doesn’t deliver much in the way of yield, it’s a little less than 1.15% with shares at $143. That said, there is absolutely nothing not to like about the payment and the outlook for future distributions. The company is only paying about 24% of the consensus earnings and the balance sheet is a fortress. The company is carrying some debt but coverage is very high, leverage is running <1X FCF, and the $1.4 billion in operating cash flow is relatively unencumbered. Along with that is a positive outlook for distribution growth. Tractor Supply has been increasing for 10 years with a 17% CAGR.

BJ’s Wholesale Club Is A Deep Value Growth Story

BJ’s Wholesale Club (NYSE:BJ) doesn’t pay a dividend but that is the only bad thing I can say about the stock. The company operates a chain of wholesale membership clubs that, quite frankly, is trading at a ridiculously deep value. The stock is trading about 12X its this year’s earnings where the 2nd cheapest comparable stock, Walmart, is trading closer to 25X earnings. Pricesmart is trading closer to 33X and Costco 37X which all imply BJs deserves a higher multiple for its roughly 18% YTD growth.

Looking at the charts, this stock may be getting ready for a multiple expansion. Price action appears to be forming a bottom at a key support level near the $36 level. Resistance is at the short term EMA and represents a 15% discount to the current analyst’s consensus. A move in the price above the EMA would be a bullish movement.

Big Lots Is Still A Big Value

Big Lots (NYSE:BIG) is one of the most surprising deep-values on the market and more so because the value has persisted for so long. The company is riding not only a wave of pandemically inspired shopping but is also benefiting from an ongoing long-term turnaround plan. Called Operation Northstar, Big Lots has been making its stores more accessible and user-friendly while trimming costs and focusing on eCommerce.

Trading at only 5.75X this year’s earnings and paying a safe 2.7% dividend Big Lots is one of the most attractive dividend stocks in the sector. Big Lots dividend is safe too. The company has a history of increases as well but hasn’t made one in several years although it could at any time. Not only is the payout ratio a very-low 15% but the company has very little debt, a very large cash pile, and generates strong free-cash-flow.

Read This Story Online |  What if I told you there's a legal way to own real physical gold and silver—and keep your gains tax-free?

No gimmicks. No shady tricks. Just a powerful IRS-approved loophole that most Americans have never heard of.

It's called a Self-Directed Gold IRA, and it's quietly becoming the go-to wealth protection strategy for people who see the writing on the wall.

When you take the next step, you could qualify for up to $10,000 in FREE GOLD & SILVER with your purchase of a qualified account. Click here to get the IRS Gold Loophole Report now |

Written by Jea Yu LIDAR technology company Velodyne Lidar, Inc. (NASDAQ: VLDR) stock has been a rollercoaster after its SPAC reverse merger on Sept. 29, 2020. The premier maker of light detection and ranging (LIDAR) sensor systems has seen a momentum surge in the segment as sentiment for autonomous vehicles improved. Velodyne founder, David Hall, was the father of the LIDAR industry. The money flow surging into electric vehicles (EVs) to charging stations to EV battery technology found it way into autonomous vehicle components which LIDAR is critical. LIDAR sensors enable autonomous vehicles to navigate accurately and safely. The rumors surrounding Apple Inc. (NASDAQ: AAPL)entering the EV market bolstered speculation LIDAR companies shooting up shares of LIDAR technology companies with Velodyne being arguably the purest play. Prudent risk-tolerant investors looking for exposure in a leading player in the autonomous vehicle revolution can monitor Velodyne shares for opportunistic pullback levels. LIDAR technology company Velodyne Lidar, Inc. (NASDAQ: VLDR) stock has been a rollercoaster after its SPAC reverse merger on Sept. 29, 2020. The premier maker of light detection and ranging (LIDAR) sensor systems has seen a momentum surge in the segment as sentiment for autonomous vehicles improved. Velodyne founder, David Hall, was the father of the LIDAR industry. The money flow surging into electric vehicles (EVs) to charging stations to EV battery technology found it way into autonomous vehicle components which LIDAR is critical. LIDAR sensors enable autonomous vehicles to navigate accurately and safely. The rumors surrounding Apple Inc. (NASDAQ: AAPL)entering the EV market bolstered speculation LIDAR companies shooting up shares of LIDAR technology companies with Velodyne being arguably the purest play. Prudent risk-tolerant investors looking for exposure in a leading player in the autonomous vehicle revolution can monitor Velodyne shares for opportunistic pullback levels.

Q3 2020 Earnings

On Nov. 5, 2020, Velodyne reported its Q3 2020 non-GAAP earnings per shares (EPS) for the quarter ended in September 2020. The Company report a loss of (-$0.06) EPS as revenue grew 137% year-over-year to $32.1 million. At quarter’s end, the Company had 175 projects in the pipeline, an increase of 34% YoY. Velodyne lowered its full-year 2020 revenue estimates to $101 million versus $109.05 million consensus analyst estimates. The Company has shipped 47,500 sensors for cumulative revenues over $615 million to date and has “the largest market share of all LIDAR companies today”, as per CEO Anand Gopalan. He clarified, “We are on the brink of LIDAR-powered autonomous revolution. The applications for LIDAR are endless and continue to grow well beyond auto. LIDAR enables broader secular trends for moving goods, moving people, smart cities, and security. Velodyne is the only company today with both breadth of product portfolio and the manufacturing capability to deliver the lower-priced LIDAR with multiple specifications at scale for real world applications… including consumer vehicles for ADAS systems, industrial robotics, delivery systems, smart cities, shuttles and many more.”

Non-Automotive Applications Flourish

The Company is a first mover in the LIDAR industry supplying over 300 customers and partnered with companies like Ford Motors (NYSE: F), Baidu (NASDAQ: BIDU), Micron Technology (NYSE: MU) and Hyundai targeting over 25 market segments beyond automotive. Robotic delivery systems are now approved in 11 states, including Texas, Florida and cities like Palo Alto and San Francisco. Last-mile applications including, “transitioning from human to LIDAR equipped robotic delivery leaves a 96% cost savings by reducing an expense of $1.60 per package down to $0.06 per package.”, stated CEO Gopalan during the Q3 conference call. The Velarray M1600 is a solid-state LIDAR sensor that provides autonomous robots with near-field perception up to 30 meters and 32-degree vertical field of view enabling them to “traverse unstructured changing environments”. It provides autonomous mobile robotic operations in warehouse, retail centers, industrial plants, and medical facilities.

May Mobility

On Dec. 16, 2020, Velodyne announced sales agreement for its Alpha Prime sensors with May Mobility, a pioneer in autonomous vehicle (AV) technology. Velodyne will provide 360-degree surround view perception technology Alpha Prime sensors for May Mobility’s entire growing fleet of self-driving shuttles. May Mobility has been operating autonomous shuttle in Grand Rapids, MI, providing over 265,000 rides since 2018. The Company plans to deploy more shuttles in 2021 in Arlington, TX, and Higashi-Hiroshima City, Japan. Velodyne CEO Gopalan summed it up, “May Mobility is demonstrating how Velodyne’s LIDAR sensors help making self-driving shuttles safe and efficient, positioning them close to public transit gaps and bottlenecks.”

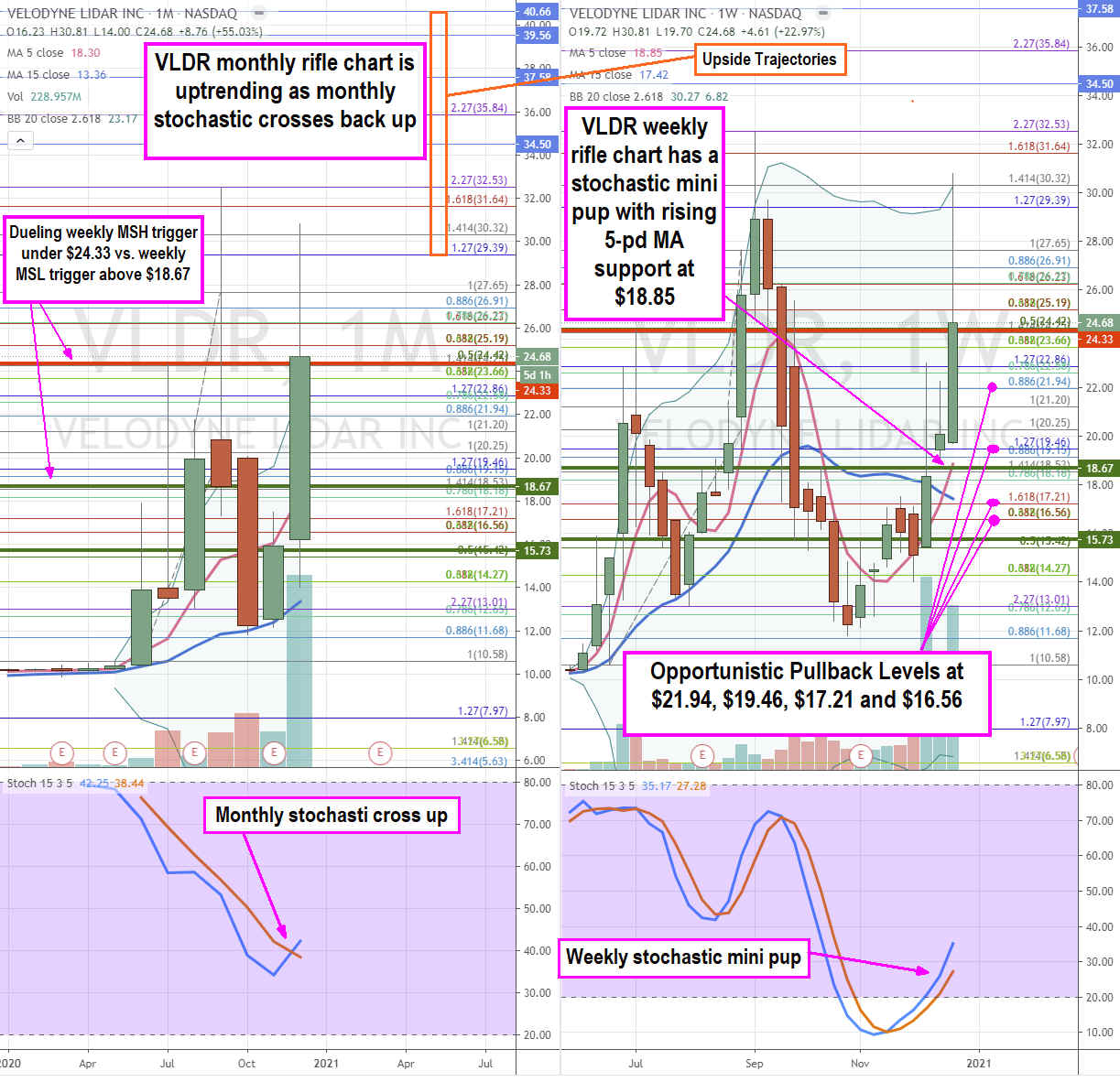

VLDR Opportunistic Pullback Levels

We use the rifle charts on the monthly and weekly time frames to provide a larger perspective of the playing field for VLDR shares. The monthly rifle chart has been in an uptrend with rising a 5-period moving average (MA) near the $18.53 Fibonacci (fib) level. The momentum is also strong with the monthly stochastic cross up at the 40-band. The monthly upper Bollinger Bands at $23.17 are expanding. The weekly rifle chart is forming a new uptrend powered by the stochastic mini pup. The 5-period MA is overlapping with the market structure low (MSL) buy trigger above $18.67. The weekly stochastic mini pup is powering the uptrend and relatively fresh as it grinds up through the 35-band. On the flipside, the weekly rifle chart also formed a market structure high (MSH) sell trigger below $24.33, formed on the earlier pup breakout in August 2020. Prudent investors looking for exposure can watch for opportunistic pullback levels at the $21.94 fib, $19.46 fib, $17.21 fib and the $16.56 fib. Potential upside trajectories range from the $29.39 fib to the $40.66 fib. Read This Story Online |  |

| More Stories |

|

|